You now know the harsh realties of the financial advisor's career and you are fully prepared.

The amount of hard knocks and work one has to go through at the beginning is worthwhile if this career is meant for the long run.

Lets take it to the next level by finding a suitable place that is nestable for a potential lifelong career.

Whether you are an advisor-to-be or an advisor switching firms, the series of interviews at FA firms and insurance agencies can put you in a whirl of excitement, happiness, confusion and leave you with many questions about the future.

The people are so nice, so friendly and so kind. The firm seems to take advisors' professional development very seriously. They meet you up so often that they are getting familiar. They want you. You are not quite sure who to join.

By the time you get to this confusion stage, your emotions run high.

At a time when emotions are high, intelligence is low.

Not exactly a good time to be making decisions.

The next thing you know it, you sign with the friendliest agency/firm to avoid further procrastination. They will fill you with guilt about procrastination anyway.

Its part of the career sales tactic.

Before you even get to the interview stage, you have to realize something very important.

You are not going for the interviews to get a job.

You are going for the interviews to interview the interviewer.

During the interview, the interviewer will tell you every single impressive thing that the agency/firm has done and will do for the advisor. Expect to hear a lot of repeats.

DO NOT count on mere words for your future, it is a HUGE gamble.

It is very easy for the salesman to glorify every single thing and promise things to you which don't have to be delivered today.

Once you have signed with the firm and gathered a pool of clients, it is going to be a pain to break away.

Imagine the opportunity cost :

You have to hunt for a new firm to join, go through tedious administrative procedures to leave the current firm, explain to every single one of your client reasons for joining the new one, apply for FAR license again at the new firm and wait for approval, go back to every single client to sign transfer forms to let you be their servicing advisor again…

Even if you want to stay in the same firm but change to another manager, FA workplace politics make it too complicated to do that. In some FA firms, it may actually be easier to leave the firm entirely than change to another manager within the same firm.

It is dumb, but that is reality.

During the interview stage you need to consider both the firm and the manager.

It is okay to go for interviews again at the same firm with different managers.

Every manager is different.

Your environment and learning path can be shaped differently under different managers in the same firm.

With so much at stake, the person who has to take interviews most seriously, is YOU.

Words from a group of salesmen (recruiting managers, directors, testimonials taken from some advisors) can build the FA workplace to be quite a beautiful facade.

Fortunately, you don't have to wait till you've gone on board to find out about whats really going on in there.

You can ask specific fact-finding questions at the interview.

We've compiled a list of interview questions for you to ask about your future financial advisory work environment.

These are the questions we would have asked.

Company-wide Features:

1. Are you offered the benefits of Client Ownership and Vesting?

Having Client Ownership supposedly means you are given the right to port your clients over to another firm in the industry when you leave.

Having Vesting means commissions follow you even when you transfer to another FA firm.

These are the most important benefits to ask about during the interview.

Life insurance agencies generally don't give advisors Client Ownership and Vesting, so you can strike those out in your interview notes when you go for the interview at a insurance firm.

If the FA firm offers Client Ownership, check if it will be stated in the contract and how it gets activated when an advisor leaves to join another:

Will the firm assign the servicing back to the advisor when he has transited to the new firm?

Or will the advisor have to go back to every client to sign a transfer of servicing form?

If it is the latter, this Client Ownership thing is just a hoax.

Cross it out and move on to the next question.

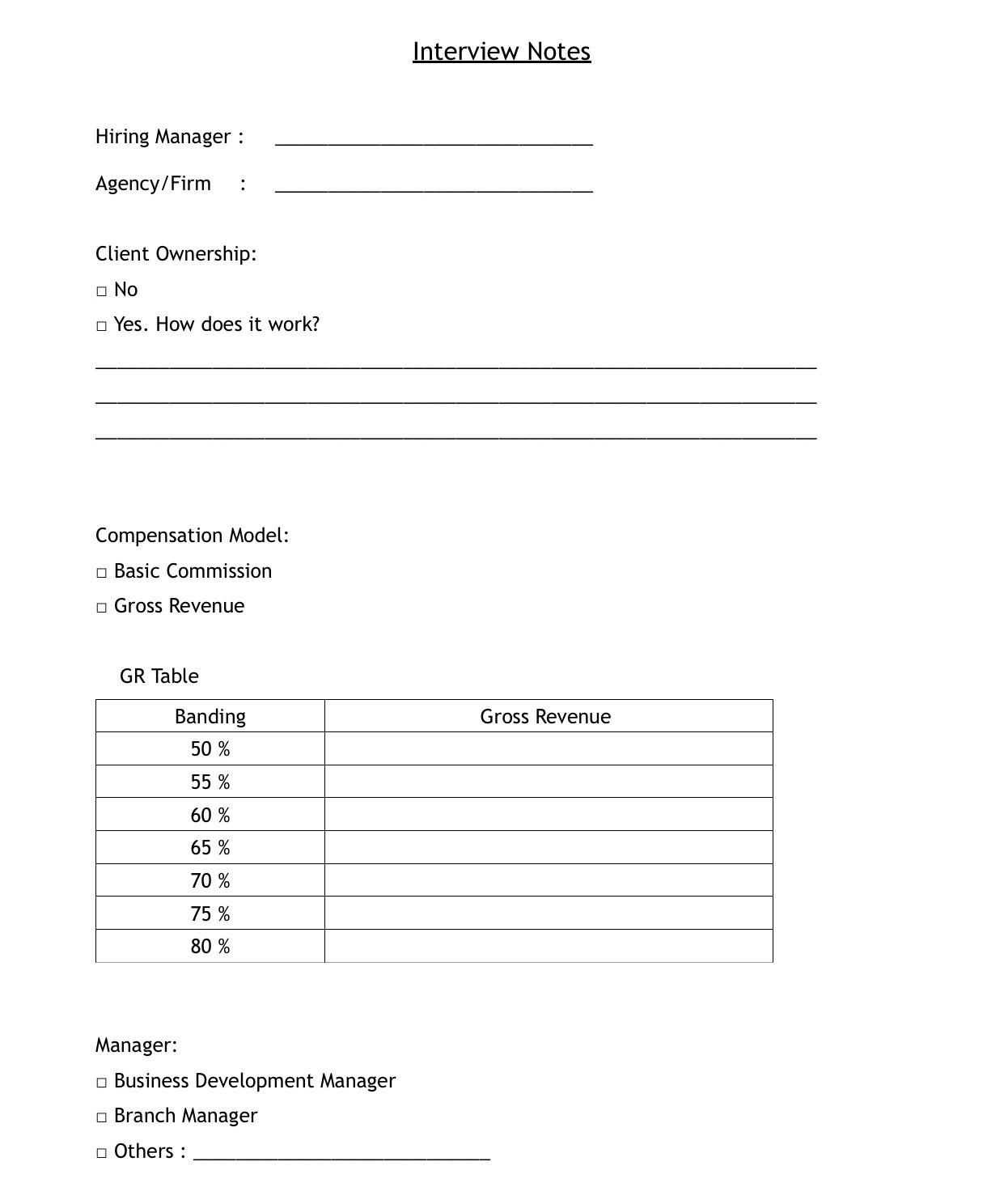

2. Compensation Model: How does this agency or firm pay you?

Predominantly there are 2 types of Compensation Model in the financial advisory sector in Singapore.

One is Basic Commission and the other is the Gross Revenue.

They are not the simplest things to understand but you have to understand them before you go for the interview, to ask clear questions.

Life Insurance agencies in Singapore presently work on the Basic Commission model.

Some FA Firms in Singapore work on the Gross Revenue model.

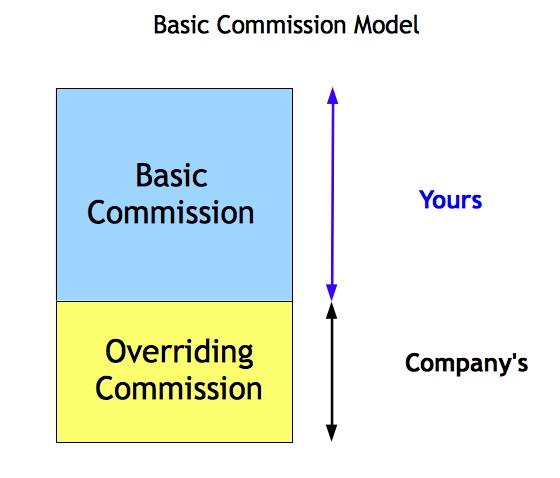

Each financial product essentially has 2 parts to its commission:

Basic Commission and Overriding Commission.

Under the Basic Commission Model, regardless of the amount of total commissions you bring in, you get the Basic Commission as your share. Your manager and the firm takes the Overriding Commission.

Under the Gross Revenue Model, Gross Revenue simply means the total amount of commissions you've brought in for you and the company.

Gross Revenue = Basic Commission + Overriding Commission

In the Gross Revenue Table, your banding shows the percentage of the total commissions i.e. Gross Revenue you've brought in that you get to keep during the banding year.

For e.g. if you've brought in $80,000 of total Gross Revenue for the year:

60% X $80,000 = $48,000 -> Your Share of Commission.

40% X $80,000 = $32,000 -> Manager's + Company's Share of Commission

Usually when newcomers enter the company, they are placed at the 60% banding level.

At 60%, the amount of commissions an advisor receives is around the same as under the Basic Commissions Model.

To draw veteran advisors from other agencies and firms, some FA firms have given these advisors a 1st year 80% banding incentive for joining the firm. Of course, this special offer is not available to newbie advisors.

If the FA firm operates on a Gross Revenue compensation model, remember to get from the interviewer the Gross Revenue Table figures and copy them down in your notes.

Some FA firms give you a higher percentage of commission (i.e. higher banding percentage) for the same amount of Gross Revenue you bring in.

That means more money for the same amount of work that you do! So this is definitely an area to keep a lookout for.

There are pros and cons for both the Basic Commission and Gross Revenue compensation.

The good thing about the Gross Revenue compensation is the more you produce, the higher the percentage you get to keep.

The downside is you must produce that amount and more every year, for the rest of your life. If not, your banding will drop.

For Basic Commission compensation, you will always get your fixed share, banding never drops nor increases.

The 3rd kind of compensation is fee based, which isn't as common in Singapore yet.

These independent financial advisors charge clients fees for advice and return to clients commissions of financial products clients acquire through them.

Manager and training related questions

1. Is your manager hired by the company or is he/she an entrepreneurial manager?

The above might sound like a odd question but it has its relevance.

Before going there, at the beginning of the interview first check with your interviewer, if he/she is going to be your manager when you join.

If he isn't, skip the 'manager questions' till you meet the actual recruiting manager.

Typically, Life Insurance agencies don't have managers on payroll to manage teams so you can safely strike that out in the interview toolkit if your interview is at the insurance agency.

At FA firms, they have both hired managers and entrepreneurial managers.

Hired managers take a monthly pay check from the FA firm and entrepreneurial managers take a cut of the total commissions you bring in.

Hired managers have titles like Business Development Manager (BDM) and entrepreneurial managers have titles like Branch Manager (BM) or Branch Director (BD).

I have heard far too many advisors complain about managers who are on payroll.

One of the complaints is that these managers do not spend time to address advisors' concerns if the concerns are not within firm's key performance indicators (KPI).

Aside from spending time with advisors, hired managers have to do many things for the firm like recruitment, event planning, project management, administrative work, trainings etc.

Attention is already divided from day one.

|

| Manager Hired By FA Firm |

|

| Manager Not Hired By FA Firm |

2.

i) How many no. of years experience does your manager have in his financial advisory practice?

ii) Is he still practising financial advisory?

iii) When did he last close a client?

(i) Years of Experience

It is important to find out about the manager's financial advisory sales background. If the manager has very little or poor relevant experience, like maybe 1 or 2 years doing financial advisory work or not successful at being a financial advisor, there isn't much to learn from him/her.

After you're done learning from him, he will eventually just be an admin person to you, signing your forms and asking you about your production every week.

If you are looking for a manger who can be your mentor, such a manager is not suitable for you.

Anything less than 3 years of financial advisory work experience is considered little ( for a manager ) in our opinion.

Another common complaint of hired managers is that they have little or poor financial advisory work experience.

It does make sense, its hard to fathom experienced and high earning advisors and managers wanting to take a salary. That would mean a pay cut.

There are also managers who have been in the industry for many years.

BUT they could have been in the industry since the 1980s and only practiced for a few years before being a manager. So, always ask specifically the number of years they have done financial advisory.

(ii - iii) Financial Advisory Practice & Last Closed Client

Some managers have many years of experience in insurance sales, but the last time they did sales was 10 years ago.

Besides staying relevant with financial advisory knowledge, one needs to stay relevant with clients as well. It is a people business after all.

The best manager to have is one who still meets new clients. Even if it shaves off some time for you the advisor, his relevance in the financial advisory field will be immensely valuable to you.

In the whole financial advisory industry, whether you are in a upcoming FA firm or an established insurance agency, it is very common to have managers teaching a lot of things that is based on theory or from books. You will also notice that they spend most of their training on motivational content.

To be practical, adding motivational content in trainings is a good way to kill training time and it is very easy to prepare.

Step 1: Go to Kinokuniya grab some books

Step 2: Go online and surf YouTube videos

Step 3: With content from the books and videos, generate a 2 hour training complete with a group discussion thrown in at the end.

Even a secondary school student is capable of facilitating such a training.

Will you choose to learn driving from someone who last drove 10 years ago?

Will you learn from someone who teach you how to drive from the driving theory handbook?

Do you expect motivational quotes to miraculously transform you into a F1 driver?

If you will not entrust your driving lessons to someone like that, will you entrust your life career to a manager who mentors you the same way?

3. Ask the manager to show you a sales presentation.

Before going to the interview, check out the firm's website and read through their scope of financial planning for the clients.

Pick an area that interests you, for e.g Corporate financial planning : Buy-Sell agreement for the Business Owners.

Politely ask the manager if he/she can show you a role-play of the presentation, with him being the advisor and you as the client.

If after you've seen his presentation, you are enticed to find out much more, you know you will be able to influence many others to feel the same way too.

If the presentation leaves you confused and clueless, it is not a good presentation.

A good presentation is one that makes complex things simple, not one that makes you feel stupid because its too complex.

If the presentation is too cheesy or too boring, you can't imagine yourself replicating it, this is not the manager to join either.

It is important to see a live example presentation because it is a sneak preview to how this manager will impart financial advisory work skills to you in future.

Whatever the manager shows you is likely to be whatever you are taught to show clients.

If you are not impressed, don't join.

If the manager rejects you because it is not his area of specialty, ask if he can show you another presentation which he specializes in.

If you are rejected for a reason like 'Its is too advanced for you', there can be 2 possible real reasons.

1. He is not confident enough to show you the presentation.

2. He might be one of those managers who will always tell you to concentrate on your 'bread and butter' and cap your learning curve because he has already let his learning curve plateau and is unwilling to advance. Even if he sounds like he is very knowledgeable, do not be taken in, people in this industry are very good at projecting a facade. Many times their knowledge comes from repeating other people's client experiences and cleverly passing other's experiences as their own.

Hired managers are often guilty of letting their learning curves plateau. The fact that they gave up on sales to take a salary already speaks volumes.

When you advance quickly and possibly advance ahead of them, it makes them look bad the day they have to say to you these 3 words: "I don't know". In the financial advisory industry many people will never do you the favour of saving your time and tell you "I don't know." Compared to your time, their face is more important.

Whenever you ask an advisor, manager or director a work related question, if they have the answer, they will never hesitate to impress upon you their wealth of knowledge.

However if they are doubtful of their answer, they will never answer you straightaway or just say a plain "I don't know".

They will always ask you Why you are asking that and ask all kinds of questions to skirt around the topic. After 15 mins you realise you still don't have the answer and have wasted your time and energy.

Also, when will you ever be good enough for something 'advanced'?

There are advisors who have been with their firms for 10 years and they still hear the same thing: "Its too advanced for you, just focus on your bread and butter."

You don't want to commit 10 years of your life to find out you have been fooled.

Insist that he shows you that presentation, if not just strike this manager out of your list.

4. Ask the manager about the trainings you are interested in and if you can sit in.

Far too many FA firms claim they have world class trainings and are keen on advisor's professional development.

Yes, they are, that is before you join them.

If the manager tells you about world class trainings that the firm provides and advanced financial advisory work the firm takes interest in educating the advisors on, do one very important thing.

Ask to sit in one of the trainings.

If you can't, do the next most important thing.

Mingle with the firm's advisors and ask if there are such trainings and what exactly do they do in there. If it all sounds really vague and iffy, definitely discount those trainings as part of your reasons to join.

There is no perfect manager or agency/firm but knowing what questions to ask will help you filter the ideal manager and firm to join so that you can have a head start compared to others who join based on blind faith.

However, a head start does not guarantee the financial advisor long term success.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}